BlackRock’s GIP Deal: Is Infrastructure Cool Again?

On January 12, global asset manager BlackRock announced it would pay $12.5 billion in cash and stock to acquire Global Infrastructure Partners (GIP), an infrastructure asset management firm. It’s our view that the deal is significant for several reasons that bode well for investments in public infrastructure. Find out why!

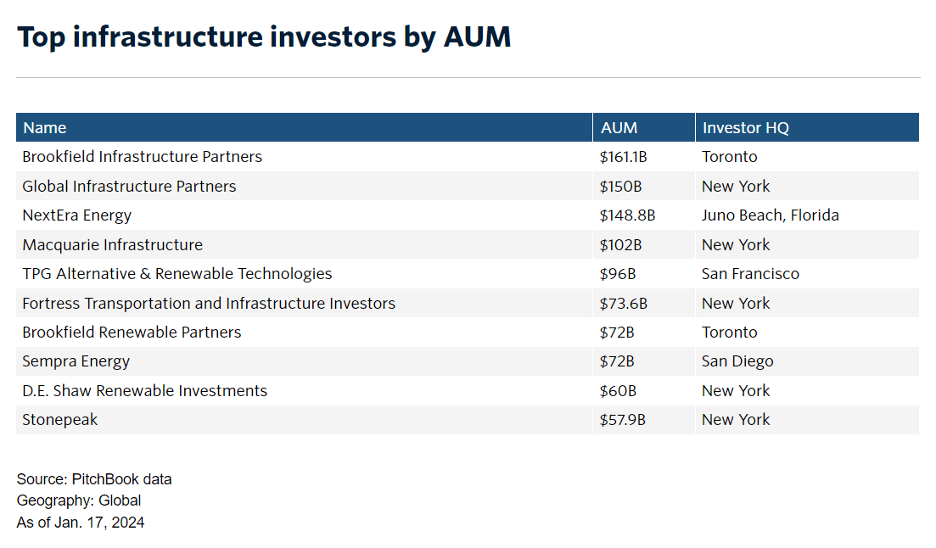

The deal combines GIP’s $100 billion in assets under management (AUM) in a portfolio encompassing energy, transport, water, waste, and digital infrastructure with BlackRock’s $50 billion infrastructure platform, resulting in the second largest global infrastructure investor, according to PitchBook Data.

The acquisition of GIP marks the company’s largest acquisition in over ten years. BlackRock is a global asset management behemoth with nearly $10 trillion AUM and 20,000 employees. The firm has traditionally focused on publicly traded debt and equities. It offers a comprehensive array of actively and passively managed mutual funds (including index funds and ETFs, which have been a major growth driver in recent years). GIP has 400 employees and manages a portfolio of public infrastructure like toll roads, pipelines, and airports.

What are Alternative Assets, and Why Are They Important?

Alternative assets refer to categories of not-publicly listed assets, such as private credit, private equity, hedge funds, and infrastructure. Historically, the major investors have been large institutions, but there is growing demand among retail and high-net-worth individual investors for access to alternative funds.

Historically, private equity and credit offer the potential for greater gains than listed securities (partly due to an illiquidity premium). Additionally, the number of listed public companies has declined as fewer companies go public, while private investments are attracting growing institutional capital allocations. In recent years, there has been an increase in traditional asset managers such as Vanguard, T. Rowe Price, Macquarie, and others moving into offering alternative investment products to their clients. In 2022, AllianceBernstein acquired alternative investment manager CarVal Investors, while Franklin Templeton acquired Lexington Partners.

However, with the recent increase in interest rates, private equity will be challenged to replicate the returns of a low-interest rate environment, so investment inflows have slowed.

Infrastructure Stands Out Among Alternative Asset Classes

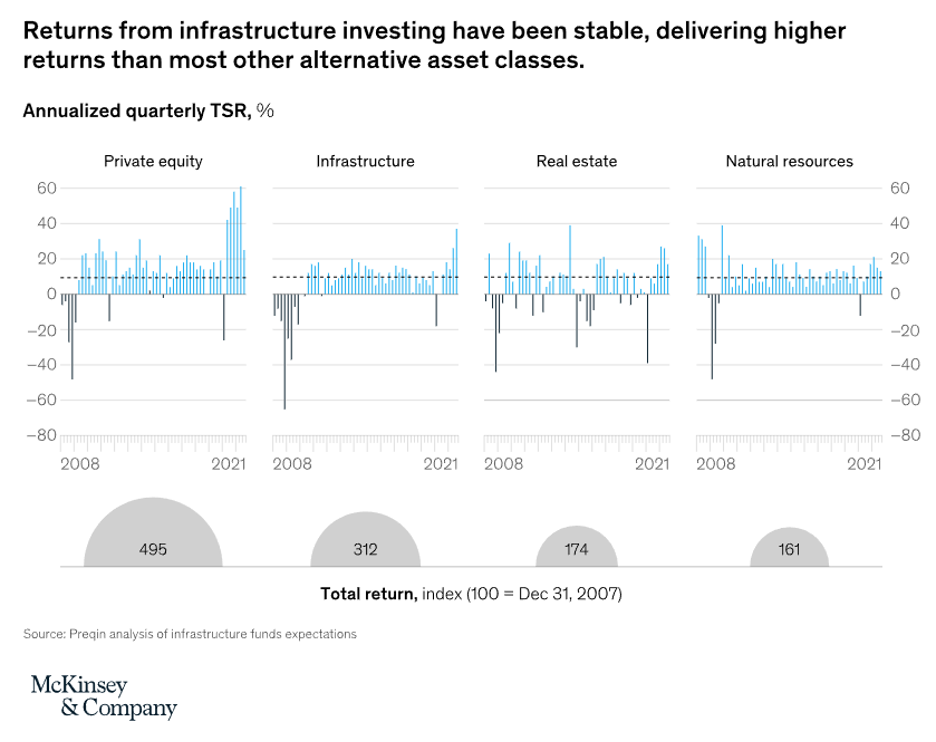

Infrastructure is an increasingly attractive alternative investment in an environment of higher interest rates and market volatility. Infrastructure offers resilient income and capital appreciation across market cycles as an asset class, delivering higher returns than other alternative classes. The nature of the infrastructure business customers (such as pipelines, toll roads, and airports) is that there is a lot of longer-term visibility and predictability in the annual revenues (versus the volatility of PE and hedge funds).

McKinsey predicts infrastructure funds will more than double to $2.5 trillion AUM by 2027. There have been other M&As in the space recently. In 2023, Luxembourg-based PE firm CVC Partners acquired infrastructure manager DIF Capital Partners, while Investcorp took a 50% stake in Corsair Capital’s infrastructure business.

From a fundamental standpoint, the transition to low-carbon energy and the increasing digitalization of the economy will drive long-term investments in infrastructure. Additionally, higher interest rates and government deficits create opportunities for private investors to invest in infrastructure through public-private partnerships.

Fulfilling BlackRock’s Long-Term Focus on Expansion into Alternatives

BlackRock has been focused on accelerating expansion into private markets for some time, and the firm’s 2024 Private Market Outlook identified the infrastructure sector as “having a moment.” According to FT, the company had been looking for alternative assets for a long time; the board had considered potentially looking at Carlyle. Also, it held early talks with another PE firm. Once the deal is completed, the CEO and co-founder of GIP, Bayo Ogunlesi, will run the infrastructure division and will also sit on BlackRock’s board of directors.

BlackRock’s move into the combined infrastructure business is consistent with its more activist goal to achieve net zero greenhouse gas emissions by 2050 while supporting investments into digital infrastructure and global supply chain hubs. Some have also expressed views that BlackRock could become a competitor to China’s Belt and Road Initiative, as the combined entity has the scale to undertake large restructuring projects. At the same time, close ties with the U.S. government could strengthen the ability to compete for international deals.

Infrastructure Investment Readies for Prime Time

Momenta believes that the BlackRock/GIP deal is meaningful because it elevates the strategic importance of infrastructure as an asset class (and not just for its common utility). This is part of the trend of traditional asset managers expanding into alternative asset classes (which also carry higher management fees) while opening up future investments to a broader base of investors. GIP’s specific expertise also provides the capability to drive value from management expertise beyond strict financial engineering. Lastly, the deal helps to validate the inherent value of infrastructure as an asset class and as a long-term investment theme, as major projects will have increasingly flexible options for funding.

Momenta is the leading Industrial Impact venture capital firm, accelerating digital innovators across energy, manufacturing, smart spaces, and supply chain. For over a decade, our team of deep industry operators has helped scale industry leaders and innovators to improve critical industries, the environment, and people's quality of life.